The school bell rings.

Time for your Calculus class. Then English. Then Money Empowerment.

Wait, what?

Okay, so maybe the last option isn’t one of your high school classes. However, things like college, a full-time job, and your own apartment are not too far away and you need strong money skills to be able to manage whatever life throws at you.

Here are 6 key money tips to help you crush money management (no Money Empowerment class required).

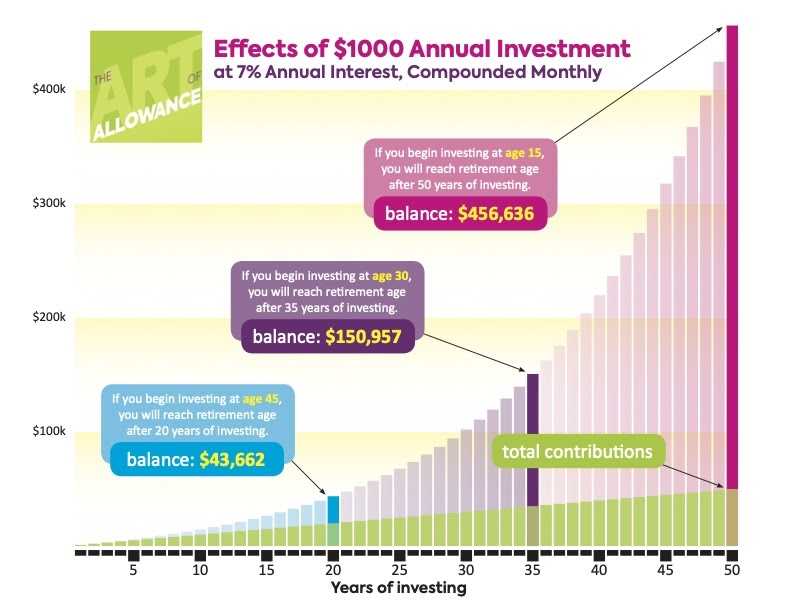

1. Understand compound interest

Compound interest is a magical finance tool (no magic wand or Hogwarts letter required). It basically means that you earn more than you invest over time.

Think of it this way: you post a TikTok video. A few people watch it and then a few more. The video generates or “compounds” views the more it’s shared. Before you know it, your video has thousands of views.

In finance, compound interest means that your money works for you – even if you’re asleep! For example, say that you deposit money in a standard mutual fund (aka a type of investment that lets you invest in stocks, bonds, etc.).

Interest (aka more money) is added to your original dollar amount by the day, week, month, or year.

Over time, your original dollar amount grows in value as your appreciation also appreciates. It’s like an appreciation party!

Time is your best friend with compound interest…the earlier you start taking advantage of it, the more money you can earn. Compound interest + time can literally make you a millionaire!

2. Live below your means

Live below your means. In other words, don’t spend more money than you make. This way, you always have money for the things you need AND can save for the future.

This money habit isn’t easy. Our brains are hard-wired to want the same stuff as our friends or family members. We feel a need to match appearances and keep up with other people’s lifestyles.

Think about it: when we scroll through Instagram and Snapchat, we see people wearing designer clothes, driving a sports car, or showing off that signed poster from Billie Eilish. It’s natural to want these items too!

It can also be smaller things that make us want to spend more than we make; like your friend’s perfect shot of that California sushi roll or the heart-shaped foam in that $4.00 latte.

Hungry yet?

So we purchase these items ourselves – even if it’s on a credit card or it means we won’t have enough money for expenses at the end of the month.

This concept is known as “Keeping Up with the Joneses.” Nah, we don’t mean the Joneses who actually live down the street from you. “The Joneses” can refer to anyone who causes us to want to spend more money than we make.

The problem is that there will always be Joneses to keep up with. No matter how wealthy you may be, there’s always someone with more money. Spending more than we make and going into debt becomes a never-ending cycle! This is why it’s important to make purchases that we can afford.

Splurging every now and then is definitely okay…but just make sure that you actually want the item and aren’t just basing it on the Joneses!

3. Use money as a tool for your well-being

Money is great. It lets us do things like travel to Hawaii, buy that pair of Converses, and drive a sports car (hopefully an affordable one ;). It also lets us live secure lives.

Now, it’s important to note that money should always be treated as a tool to create a happy life, not as the goal of life itself. If we view money as the ultimate end-all, be-all, we’ll never have enough.

BUT there is a direct, positive relationship between earning more money and our well-being. In fact, recent research shows that earning more money leads to greater well-being.

The same research shows that higher incomes (aka $75K per year and above) are connected with both feeling better day-to-day and being more satisfied with life overall.

As you earn more, research also tells us that we can use our money in specific ways to make us happier. These include

- Buying experiences (ideally, with others)

- Indulging ourselves from time to time (but not always)

- Buying ourselves time

Let’s look at an example of buying ourselves time (aka making a purchase to free up time). Say that you’re spending hours every week studying chemistry.

You want to make a good grade in the class but you’re also missing out on doing things with your friends in the afternoons. You need more time. In this case, you might pay for a chemistry tutor to help you understand concepts faster, freeing up your time for other activities.

This example perfectly sums up using money as a tool. It’s definitely a good thing to earn more money, but it should be viewed as a tool for helping you live a happier life.

4. Invest intelligently

To invest intelligently means two things: 1. to put your money or time into something worthwhile and expect a benefit in the future.

Say that you want to score more soccer goals. If you invest the time to practice, you can achieve this goal (literally and figuratively) over time.

But investing intelligently also means to 2. understand our weaknesses when making investing decisions.

Why? Humans are TERRIBLE investors.

As humans, it’s easy to assume that we’re good at predicting the future. But here’s the thing: most of us don’t have a crystal ball and we normally choose possibility over probability.

For example, let’s say that your favorite singer is releasing their fifth music album. This artist has ALWAYS released their music in April. Since we base many decisions on patterns, you might predict that this album will also be released in April.

It’s definitely possible that this artist will release the album then, but it’s not probable just because there’s been a pattern of April releases *cue a song from your favorite singer.* At the end of the day, the album release depends on a lot of factors and can be quite random (looking at you, T-Swift).

In short, just because something is possible doesn’t mean that it’s probable. It’s this type of thinking and human biases (aka being in favor of or against a particular thing) that make humans pretty poor investors.

Now, does this mean that you should stash money under your mattress and forget about investing? Not at all. As we learned about compound interest, investing can make you a millionaire over time.

Investing intelligently simply means that we recognize our flaws as humans and know that we actually can’t predict the future. This awareness helps us make smarter, simpler investment decisions such as limiting how many stocks we pick or avoiding putting our money in the lottery.

5. Weigh all costs

As much as we might like the idea, rarely do we get something for nothing. Even that free T-shirt you got at a Ariana Grande concert isn’t actually free. Someone had to pay for it.

Everything has a cost including how you spend your time and how you spend your money. These costs affect our lives every day and it’s important to weigh costs to make sure we’re making the best possible decision for our future.

Think of costs in terms of time. Maybe you want to buy a new video game that just came out. You know that you’re going to have to wait in line for hours to get the game on Saturday.

Now, your friend is also having a HUGE party the same day. All of your friends will be there. You then have to weigh the costs: how badly do you want the video game vs. hanging out with your friends?

There’s no right or wrong answer here. It’s simply being aware of what you’re giving up and deciding if the costs are worth it.

The same concept applies to your finances. For example, if you decide to buy a new pair of Airpods, you’ll have less money to go into your car savings fund. Or vice versa, if your money goes into your car savings fund, you might have to wait on the Airpods and get a regular pair of headphones instead.

Carefully weigh the costs of your time AND money decisions to determine if they’re worth it.

6. Make good debt choices

You’re probably familiar with bad debt. If you’re not, picture trying to carry an elephant on your back and you’ll quickly get the idea.

Think of bad debt being things like racking up a huge balance on a credit card with a 21% interest rate. Or taking out a high-interest personal loan to pay for a trip to Antarctica. This type of debt can quickly damage your finances.

But did you know you can make good debt choices? Good debt can be used to build wealth or increase your income over time.

Say that you’d like to buy your dream house one day, complete with a huge pool, home theatre, and maybe a video game room. This purchase requires a good credit score (hint: 680 and above is considered a good credit score while 800 and above is considered excellent).

To build your credit, you can use a low-interest credit card and make your monthly payments on time. You can even earn reward points! In this case, debt is okay as long as you’re careful and can always afford to pay off the balance at the end of the month.

The same applies to taking out a mortgage for that dream home. It’s best to save 20% for the down payment, but you can take out a mortgage to afford the rest of the house and become a proud homeowner. You can then make monthly mortgage payments. The mortgage is a good debt choice because a home is something that can increase in value!

When used wisely, good debt can actually help you reach any S.M.A.R.T. financial goals you’ve set. Debt, like money, is a tool that can be carefully used to build the life you want.

Be smart with your money.

Money empowerment starts right now with you. Use these six tips as the foundation for making smart money decisions – in high school and beyond!