I recently reconnected with a high school friend whose older daughter, Sam, is now in college. When she was accepted Early Decision to her top choice, he immediately realized:

“Oh, crap! She’s heading to college. And she doesn’t even know how to change a tire.”

He hastily created “Sammy-versity,” his makeshift “College of Life,” to ensure she knew not only how to change a tire but also how to do laundry, make a few important meals and balance a checkbook. (Incidentally, I’m not sure today’s digital natives will ever need to balance a checkbook. I haven’t in years.)

Inspired by “Sammy-versity” and the reality that my own daughter is heading to college, I thought it would be helpful to create a list of financial concepts I wanted to be sure she understood before she began “adulting.”

The List

Let’s begin with the full list, and then I’ll jump into each financial concept in a little more detail. The first two concepts come from my grandfather, to whom I dedicated my book The Art of Allowance: A Short, Practical Guide to Raising Money-Smart, Money-Empowered Kids.

These are essential concepts that I hope my kids grasp earlier than I did. This list also serves as a sort of personal wish list. I wish I’d understood these concepts much earlier in my life.

- Compound interest is the key to money, friendships, skills and just about everything.

- Live beneath your means, and you will avoid many of life’s headaches.

- Money is a tool you use to help you craft whatever life you pursue.

- Whether opportunity costs or time costs, everything has a cost.

- Invest intelligently by understanding yourself and human nature.

- Make good debt choices for your situation.

Of course, making good choices pertains not only to debt but also to all of these concepts. Using money is all about making choices.

And, sure, I can hear more than a few of you already exposing the flaws of my shortlist:

“What about ‘paying yourself first?’”

“You missed dollar cost averaging!”

I didn’t even include one of my wife’s favorite quips (although she doesn’t take credit for it): “You and your company are even on payday.”

Please don’t despair. You may sheath your swords.

Allow me to unpack each of the six concepts, and I think you’ll find these ideas living within them.

1 — The Real Power of Compound Interest

“All the real benefits in life come from compound interest.”

— Naval Ravikant [Bold is my emphasis.]

For years I’ve struggled with how to emphasize to kids the incredible power of compound interest.

Invoking Charlie Munger? Crickets.

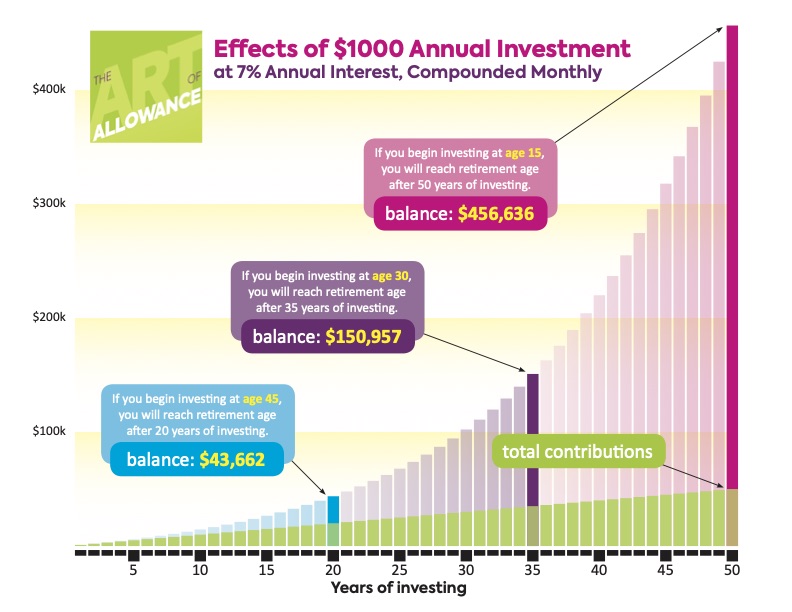

Showing them this beautiful graph we created? It helps, but there’s still work to do.

How about the shortest compound interest video ever? Again, helpful. But how are these young humans possessing not-fully-formed frontal lobes walking around with an air of invincibility going to grasp benefits that won’t appear for 30 years? We are biased to value present money much more than future money. It’s called hyperbolic discounting, and it requires money mindfulness to overcome.

Even emphasizing that “understanding compound interest” was my grandfather’s number-one piece of advice the day I graduated college didn’t do the trick. He came from no money, and although he made a good living as a commercial pilot, it was his respect for this concept — compound interest — that made him a millionaire.

Enter Naval Ravikant, angel investor and modern-day philosopher (also now the subject of a new book, the Navalmanack). Per the quote at the start of this section, Naval points out that compound interest isn’t just about money. It’s about life. Friendships, skills and cash all build slowly until seemingly all at once you say to yourself, “Hot damn!” How did I get so lucky to have these relationships? When did I learn to play, paint or write so well? Where did this nest egg come from?

Putting compound interest in a broader context makes it more meaningful.

Couple this insight with this video by money psychology expert Morgan Housel. His helpful, powerful analogies can help uncover the power of compounding for the younger set.

2 — Live Beneath Your Means

“We Americans have about three times the space we had about 50 years ago.”

— Graham Hill, TED Talk entitled “Less stuff, more happiness”

The average home size has more than tripled, while the average household now has fewer people.

How did this happen?

It’s those dang Joneses. The ones so many humans are trying to keep up with.

Don’t try to keep up with the Joneses. You have no idea if the luxury-car-driving Jones next door is living paycheck to paycheck. But let’s say you do catch up. There will always be another Jones to chase. It’s an unwinnable and unfulfilling game.

I shoehorned the all-important mantra — “Pay yourself first.” — in this section because it’s a solid strategy for avoiding the Jones trap. If you stow away large amounts of your gains as you advance in life — whether from salary or due to passive means — and reinvest them in yourself or others, then you’ll live a more fulfilled life.

Of course, stop to reward yourself from time to time. Be sure, though, that you are the one making purchase choices and that they‘re not being made for you. Why are you buying a new Porsche Cayenne and not a Honda CR-V? Are you trying to keep up with someone? Will the driving experience feel different in two weeks? A month?

As parents, we can make sure that our kids are aware of these sometimes hidden trade-offs. They see us blow $25,000 on a new car and then tell them to save for a smaller item — a pair of shoes, a video game system, whatever. To them, this must seem like a drop in the bucket and look like perhaps we’re hypocrites.

Rather, we should explain our reasoning — the family needed a car, and we decided to buy a pre-owned vehicle instead of a new one. Or that we bought a value versus a luxury brand. Giving voice to our choices helps our kids understand that we’re making smarter choices than they might imagine.

Living beneath our means makes us much more resilient to economic shocks too, like the one we’re experiencing amidst this pandemic.

This concept cracks the top two on this list because it took me so much time to figure out.

3 — Money Is a Tool (And Nothing More)

“Money isn’t a material reality – it is a psychological construct.”

— Yuval Noah Harari, Sapiens

A fundamental truth that I want my kids to recognize before they head into the world is that money for the sake of itself is never satisfying. Can money be used as a tool to satisfy desires? Does money give you more options to travel? To live the life you want? Yes, yes and yes.

This doesn’t mean that you don’t have options without loads of money. It just means that specific ones (such as second homes, higher-end cars or political influence) are fueled by money. Plenty of options, and perhaps the most important ones (like your own reasoned choice and living ethically), are independent of money.

It’s also vital that children recognize that although money won’t buy happiness or love (something young Lennon and McCartney figured out), it does correlate with life satisfaction. More importantly, the lack of funds leads to comparatively more misery.

Money matters, but not in an intuitive way. You need enough of it, but this pursuit often leads us to hop on the hedonic treadmill — one that allows for no rest. The speed is continually increasing.

To keep up with the Joneses. Dang it! Joneses again!

We need to establish systems that allow us to avoid misery, not be slaves to our desires.

In short, we want our kids to understand that money is a tool. Nothing more. A hammer drives in nails. It’s terrible at securing screws. Money buys you things. It’s awful at securing happiness.

4 — Everything Has a Cost

“Remember: even what we get for free has a cost, if only in what we pay to store it — in our garages and in our minds.”

— Ryan Holiday and Stephen Hanselman, The Daily Stoic

When I went to college, a credit card company offered me a free t-shirt. I immediately signed up. What was there to lose? I got additional spending power and something for nothing.

I didn’t realize that we rarely get something for nothing.

One minor cost of a free t-shirt was that it added more choice to my morning routine. I didn’t realize it at the time, but we have only a small daily store of energy to make choices. Adding a t-shirt to the list of answers to my daily “What am I going to wear?” question helped drain that mental battery. And though this one “free” decision might have drained very little juice, lots of these small decisions can add up.

Before we know it, we’re being taunted by those items we bought on sale, the stuff we picked up at conferences and those gifts we knew we didn’t need but kept anyway. We tell ourselves, “I’ll get to that pile tomorrow,” not realizing how mentally draining these choices can be.

We should introduce our kids to the powerful idea of sub-accounts from a young age. For example, there’s power in the Share jar of a three-jar Share, Save and Spend Smart system. This physical form of a sub-account allocates money for giving, so donation decisions aren’t weighed against personal spending ones.

Sub-accounts change the opportunity cost calculation. Now that extra thirty bucks is going to the DonorsChoose classroom or the homeless support fund drive. It can’t be spent on a new video game controller. Sub-accounts remove the personal consumption value (for which our bias is high) from the equation.

Time costs matter as well. I know many folks who trade a long commute for additional square footage without considering all the costs involved. The commuting cost is the easy one. But how about time, the one resource that cannot be replenished? And even though you can make that time productive with podcasts or batch calling, your driving draws down your decision-making battery. For much more on time costs, my conversations with time-tradeoff genius Ashley Whillans can help: here and here.

Also, what if all this commuting means you’re too exhausted to be present in the time you spend with your kids?

Everything has a cost.

5 — Invest Intelligently

“Unlike other animals, humans believe we’re smart enough to forecast the future even when we have been explicitly told that it is unpredictable.”

— Jason Zweig, Your Money & Your Brain

You might be thinking, “Uh…of course.” This point — to invest intelligently — seems so obvious that you might be wondering why I included it in a list of six key points our kids must understand.

I’ve included it because it is extremely difficult for us to invest intelligently when we fail to recognize our biases. Mister Rogers’ Neighborhood and Sesame Street taught us that we’re special. This truth about investing teaches us something else: Most of us aren’t very good at it.

We are novelty-seeking and persuaded by the majority. We choose possibility over probability, and we are addicted to anticipation more than to the receipt of money made. We are terrible at predicting the future and what will make us happy. We value the present over the future, and we often compare ourselves to others. (Remember the Joneses?) We believe there are patterns where only randomness exists, and, to top it off, we tend to think we’re better than average in all of these areas.

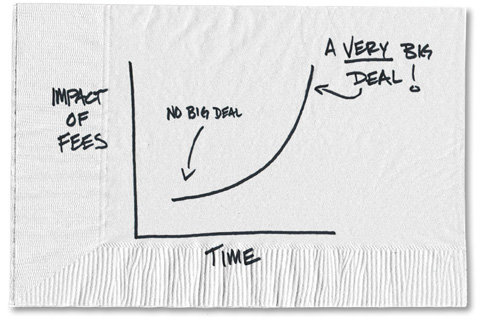

Knowing our flaws can help us make smarter, simpler investment decisions, like limiting our stock picking — our “mad” money — to 10% of our portfolio and investing in set-it-and-forget-it mutual funds. It also helps to understand how fees affect performance. Author Carl Richards of The Behavior Gap sums it up on a napkin.

The irony is that our kids must understand that they are likely to be intuitively poor investors in order to learn to invest intelligently.

6 — Make Good Debt Choices

Like money, credit cards are neither good nor bad. They are tools to be used. If you decide that owning a home is something you’re interested in doing, then you’ll most likely need a loan. You’ll get a better one with a good credit score. Therefore, you should build your credit, and credit cards are a useful vehicle through which you can do that.

Our kids begin with debit-only cards to avoid the mistake of buying something for which they have no money. They may never want to move on from this approach. That will be a choice that we should want them to make for themselves. If they understand points 2, 3 and 4 from this list, then they’re unlikely to get themselves into much trouble.

I am biased towards homeownership (My wife’s a realtor.), but that doesn’t mean that mortgage debt is good debt. It just means that it’s a debt with which my wife and I are comfortable. The associated risk is worth it to us in order to realize the potential gains. It helps that the United States is also biased towards home ownership and allows us to take a mortgage deduction and pay lower taxes on long-term appreciation. The latter, of course, is not guaranteed and is certainly variable. Incidentally, understanding risk almost made the list. Let’s call it point 6a.

If our kids leave the nest knowing that debt, like money, is a potential tool to be wielded, then we’ve done well. Of course, this includes teaching them that credit card debt should always be addressed as a short-term solution!

Money Empowered!

The Art of Allowance’s subtitle is “A Short, Practical Guide to Raising Money-Smart, Money-Empowered Kids” because I view money empowerment as the ultimate goal.

The journey to money empowerment is lifelong, and incorporating these six points into your children’s system of beliefs can help light the path.

They will make mistakes. And that’s ok. We want our kids to begin learning money smarts early so that they make “lower-stakes” mistakes — when they’re not life-altering. To be sure, the journey will be rocky, even with complete comprehension of this list. Recognizing our flaws requires us to understand ourselves better. This is challenging and takes years.

With these lessons learned, I hope my kids — and yours — can be resilient and use money as a tool to live happy, productive, fulfilling lives.

John