So you’ve been following the one-dollar-per-week-per-age-of-your-child allowance system for a while. However, now you have a tween, and you feel that the time has come for her allowance to mature (whether or not you think she will). Your tweenager (Is that a thing?) is at a perfect age to start taking on more money responsibility. I call this new “upgraded” allowance that she will receive as a result the Breakthrough Allowance, and the following sections of my book for parents, The Art of Allowance, describe how to get things started with your tween, teenager or tweenager. (It’s now a thing.)

Don’t be surprised if folks not using this plan are flabbergasted by the amount of money afforded by the Breakthrough Allowance. Without context, your friends and family might think you’re completely off your rocker, as mom Melissa Disharoon discovered in an episode of The Art of Allowance Podcast. Melissa’s sister initially scoffed at the hundred bucks a week granted to Melissa’s kids, but when Melissa explained that there was a method to the madness—and that this amount wasn’t just a handout—her reasoning became clear. In fact, Melissa soon discovered that she was saving money with this new approach.

Tweens and Teens (This section and the ones that follow are taken from The Art of Allowance.)

By the time your child becomes a tween or a teenager, he has hopefully saved for several SMART goals. He has been making money choices regularly by putting his allowance into the Share, Save and Spend Smart jars. He will also have been receiving increased allowances each year commensurate with his rising maturity level. He’s feeling money-smart and slowly becoming money-empowered.

Why, then, does he look at you with such disdain? Because that’s what tweens do. And they’re good at it. The warm and fuzzy days of jars may now be coming to an end, but you’ve provided him with a pretty solid money foundation. And this is what you get in return? Raising kids is a bit like dollar-cost averaging—steady investment through the highs and lows will pay off.

Our older daughter—now a teenager—is almost always negotiating with me. She was recently developing an expensive açaí bowl habit that we didn’t want to feed. In a moment of my weakness, she convinced me to take her to Jamba Juice, where she would typically be responsible for the purchase using her new Breakthrough Allowance that I will explain shortly. I picked her up from track practice, and she looked so spent that I agreed to buy her a smoothie. Using my acquiescence as a beachhead, she launched her full-scale assault for the pricier item, begging, “Can I pleeeeease have an açaí bowl?” (Nagging or begging, which The Art of Allowance can help reduce, is like a horror movie villain. It never really seems to die.) I told her no, unless she wanted to cover the difference. She didn’t and enjoyed her smoothie. (In case you’re wondering, I don’t always prevail in these negotiations.)

[Want to know more about The Art of Allowance? Click here.]

Eventually, your tween or teen will advance to what I call the “Breakthrough Allowance.” As he moves from childhood toward adulthood, you want to help him become more responsible with more money. The way you distribute the money and his increased responsibilities should make him feel more like an adult. Again, be explicit about what you’re doing. You can tell him that both he and his allowance are growing up.

You want to continue to help your child improve at the core skills and to recognize better the impermanent excitement that stuff brings. More money and bigger things don’t change this feeling! If you haven’t already, you may even introduce investment into the mix.

None of these tasks will be simple. Nothing involving a teenager ever is. But with a plan and a commitment to raising a money-smart kid, you can help him break through to become a money-empowered young adult.

The Breakthrough Allowance

Your tween or teen is now ready for the Breakthrough Allowance, a major developmental step. She’s moving past the starter allowance detailed earlier. Her responsibilities will increase substantially. She’ll create a yearly spending plan, and her allowance intervals will change. You may even decide to incorporate a digital allowance as I explain below.

Since she is “graduating” from her starter allowance, a little celebration might be in order. Before she embarks on the next stage of this journey, commend her for the progress she’s made in learning the three core money-smart skills: saving for goals, making smart money choices and distinguishing needs from wants. Let her know this step is a meaningful milestone.

There are some obvious areas of responsibility for your burgeoning money maven: clothes, communication, gifts and food. Don’t let the “food” category scare you. I’m talking about bringing versus buying school lunch, not raising her own farm animals. (Although that undertaking would certainly teach her responsibility.)

You’ll be increasing her total allowance amount substantially to accommodate for these new areas of control. The additional responsibilities of clothes, communication, gifts and food all belong in the Spend Smart domain. This time is a good one to consider using a digital allowance like the options offered via FamZoo or Current.

A digital allowance enables you to automate the allowance distribution process into virtual “jars.” You can also automate interest and matching. Part of her progression to becoming money-empowered is learning how to become digitally money-smart. Though a digital allowance simplifies the process, automation is silent, and you’ll want to make sure you continue the money conversation with your child.

I suggest you continue to nudge or mandate an “opt-in” to the Share and Save jars (real or virtual). You may decide to give her free reign, but with the increase in responsibility, keeping those nudges in place is probably a good idea. In fact, if you employ a digital allowance, then you can teach her the power of automatic deposits into Share and Save accounts so that she never sees—and isn’t tempted by—the money in her discretionary Spend Smart account.

[Want to know more about The Art of Allowance? Click here.]

Also, the overall percentage of the Share and Save “opt-in” contributions will likely go down, as she’ll be controlling much more discretionary income with the Breakthrough Allowance. Of course, it’s your Art of Allowance, and you may mandate larger chunks of money for either the Share or Save jars or for both.

Clothes

Giving your child control of clothes purchasing as soon as you can is beneficial. You’ll be shocked (unless you already have a teen) at how quickly her friends’ opinions will impact her life. Without a plan, a clothing decision swiftly becomes something for which adult input is not solicited—until the time comes to swipe the credit card.

Transferring clothing responsibility to your child helps stave off nagging for twenty bucks here and thirty bucks there. More importantly, your child then has skin in the game and will more thoughtfully consider her purchases. I think you’ll find implementing this plan will save you significant money in the long run.

I wish we’d tracked spending for clothes, communication, gifts and food leading up to the Breakthrough Allowance. I’d love to say we knew exactly how much she should budget per month on clothes. But we didn’t. I tip my cap to those parents who do.

We did sit down with our twelve-year-old at the start of the Breakthrough Allowance process to help her work through the proper monthly amount, using a spreadsheet which I created from her yearly spending plan.

Communication

If and when (okay, when) you decide your child should have a phone, she should at least pay her portion of the monthly bill. This practice is particularly easy to do if you’re using an automated digital allowance.

My wife and I typically gift our hand-me-down phones to our daughters. Some folks have their kids pay a nominal amount for used phones. Your choice. Interestingly, our older daughter would wait as long as possible to get a free phone. Though she’s more of a natural spender than her sister, she wanted to direct her money to other stuff she really cared about. And yes, she’s still learning about the impermanence of the “jolt” that stuff brings. Building this knowledge base takes time.

Our younger daughter, a more natural saver, decided she wanted a newer, faster, pricier phone with a good camera and saved for it using Save jar funds. However, she did buy a refurbished one to save herself some money.

Gifts

Adding gifts for friends to your daughter’s responsibility basket is sensible. This practice forces her to think—yep, Spend Smart —about her own gifting. Watching this change in perspective is funny. Once our daughter became the one forking out the gift money, she decided that good enough was okay.

When your child is responsible for buying gifts, they become generally more meaningful. Frankly, we all know what happens to a kid’s creative gift idea when she realizes you’ll cave and take her to Brandy Melville in the 11th hour. Adiós, plan! When the money is coming out of her pocket—or jar—a light bulb goes off. She becomes the Martha Stewart of gifting.

Food

One of the best pieces of advice offered in Ron Lieber’s terrific book The Opposite of Spoiled: Raising Kids Who Are Grounded, Generous, and Smart About Money is to have your child make his own lunch.* If you want to improve your family’s morning routine, then try this trick. It works wonders!

We made a deal with our kids—we’d buy lunch fixin’s at no cost to them. The decision whether to bring lunch or buy it at school with their Breakthrough Allowances was theirs. This system serves as an incentive against blowing money on too many school lunches—which can add up. We also included money for after-school snacks on the local boulevard with friends. These relatively small expenses can add up fast, so make sure to try to account for as many of them as possible when you negotiate the Breakthrough Allowance with your teen or tween.

I don’t, however, recommend going cold turkey and budgeting nothing for school lunches. When you first set up the Breakthrough Allowance, you’ll want your child to allocate money for a few school lunches per month. You’ll need a safety valve on those “special” mornings when your child has a meltdown, and absolutely no lunch is forthcoming. It’s only a matter of time. Be prepared!

On Budgeting

I have a secret—one I’ve already partially revealed. I’m not a big budget guy. This reality exists largely because I’ve always had difficulty sticking to a formal plan. My wife and I find reviewing spending patterns and being mindful about our spending and saving more useful.

If you are a budgeter, then fantastic! The Breakthrough Allowance helps your child learn basic budgeting. (See the spreadsheet below.) You can show him how you keep your spending under control—whether via budgeting, tracking spending or both. By sharing strategies, you will help him to discover what method works best for him and to become more mindful of his own spending habits.

Change the Frequency

When you transition to the Breakthrough Allowance, I suggest switching from a weekly or biweekly allowance payment to a monthly arrangement. Receiving chunks of money is more akin to what happens in the real world. This practice will let her experience that start-of-the-month feeling of being flush with cash (like her “paycheck” just cleared). If she blows her “windfall” early in the month, then let her feel the pain. As hard as this endeavor might be, she needs to learn this life lesson. Let her struggle to manage her money better. Don’t bail her out.

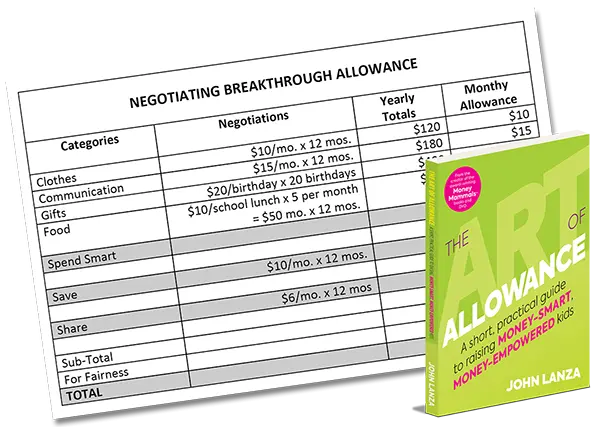

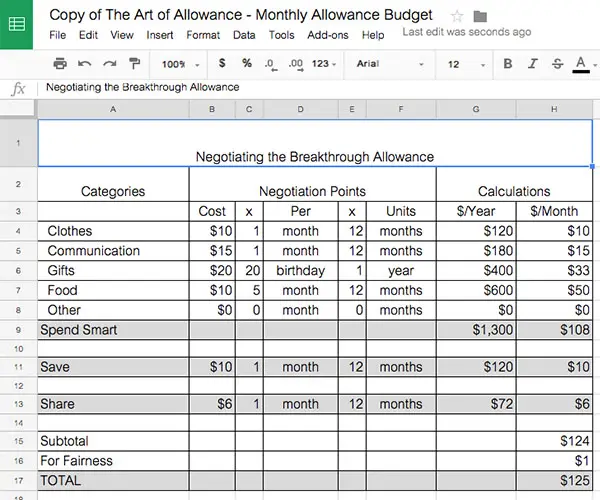

You have flexibility in making the leap from the basic one-dollar-per-week-per-age-of-your-child allowance to the new Breakthrough Allowance. And if you’re worried that going “all in” with the four categories is too much for your particular child, then start with one area—gifts, for instance. Or if you feel comfortable that she’s ready to make the breakthrough and tackle more responsibility, then pile on the challenge. Here’s an example of the simple spreadsheet I created with our oldest daughter when we negotiated her Breakthrough Allowance to be $125 per month.

Be prepared—and proud—when the spreadsheet becomes a negotiation. She will be feeling more money-empowered than when you started her on this money-smart journey. You want her to negotiate the best possible deal for herself—another great life skill for her to learn.

[Want to know more about The Art of Allowance? Click here.]

Our daughter originally came to us with an allocation of $25 for each birthday present. We felt that amount was too high, and we ended up at what we believed was a more reasonable $20 per present. When the final monthly amount came to $124, she “rounded” that number to the nearest five and asked for $125 a month “for fairness.” Maybe I’m a sucker, but her creative thinking for an extra twelve bucks per year worked on me. (Hmm…I sense a theme.) I really don’t know what she meant by “fairness” here, but her reasoning made me chuckle. She was probably still trying to make up for her perceived post-negotiation gift deficit.

As you did with the starter allowance, you’ll want to set up a periodic review of the Breakthrough Allowance on an annual or biannual basis.

You can download your own Breakthrough Allowance Google Sheet from our Art of Allowance resources page to get started today. Additionally, if you want to learn more about the Breakthrough Allowance in particular or the money-smart movement in general, then you can check out more of my blog posts, the podcast and, of course, The Art of Allowance.

John

Works Cited

*Lieber, Ron. The Opposite of Spoiled: Raising Kids Who Are Grounded, Generous, and Smart About Money (New York: Harper Collins, 2015), 155-57.